VISUAL RECURRENCE ANALYSIS

Recurrence Plots (RPs) were first described by J.P. Eckmann, S. O. Kamphorst and D.Ruelle in "Recurrence plots of dynamical systems" in 1987.

( J.P. Eckmann, S. Oliffson Kamphorst and D.

Ruelle,

Recurrence plots of dynamical systems, 1987,

Europhys. Lett., Vol. 4, No. 9, pp. 973-977 )

RP is a relatively new technique for the

qualitative assessment of time series. With RP, one can

graphically detect hidden patterns and structural changes in data

or see similarities in patterns across the time series under

study.

The fundamental assumption underlying the idea of the recurrence

plots is that an observable time series (a sequence of

observations) is the realization of some dynamical process, the

interaction of the relevant variables over time. For example, the

weather is a highly complex system with a large number of factors

that influence its dynamics, and a sequence of daily temperature

readings could be considered a realization of that dynamical

system. Another example is the stock market, -- its behavior is

determined by many factors, such as the economic and political

environment, investors expectations and individual traders’

decisions, etc. But all we typically have is the realization of

the interaction between all these factors over time, -- say, the

daily closing prices for the Dow Jones Industrial Average. In

both examples, we have a multidimensional dynamical system and a

one-dimensional output (series of scalar observations). Can we

infer any characteristics of the original system and predict its

behavior in the future given the history of its output?

As remarkable as it seems, it has been proven mathematically that

one can recreate a topologically equivalent picture of the

original multidimensional system behavior by using the time

series of a single observable variable (F. Takens, 1981. “Detecting

strange attractors in turbulence”). The basic idea is that

the effect of all the other (unobserved) variables is already

reflected in the series of the observed output. Furthermore, the

rules that govern the behavior of the original system can be

recovered from its output.

In VRA, a one-dimensional time series from a data file is

expanded into a higher-dimensional space, in which the dynamic of

the underlying generator takes place. This is done using a

technique called “delayed coordinate embedding”, which

recreates a phase space portrait of the dynamical system under

study from a single (scalar) time series. To expand a one-dimensional

signal into an M-dimensional phase space, one substitutes each

observation in the original signal X(t) with vector

y(i) = {x(i), x(i - d), x(i - 2d), … , x(i - (m-1)d},

where

i is the time index,

m is the embedding dimension

d is the time delay.

As a result, we have a series of vectors:

Y = {y(1), y(2), y(3), …, y(N-(m-1)d)},

where

N is the length of the original series.

The idea of such reconstruction is to capture the original system

states at each time we have an observation of that system output.

Each unknown state S(t) at time t is approximated by a vector of

delayed coordinates

Y(t) = { x(t), x(t - d), x(t - 2d), … , x(t - (m-1)d }

For example, let the observable time series be the weekly closing

prices for the Dow Jones Industrial Average as follows:

9/25/98 8029

10/2/98 7785

10/9/98 7900

10/16/98 8417

10/23/98 8452

10/30/98 8592

11/6/98 8975

… …

Then for d=1 and m=3, the reconstructed vectors are defined as:

Y(10/9/98) = {7900, 7785, 8029}

Y(10/16/98) = {8417, 7900, 7785}

Y(10/23/98) = {8452, 8417, 7900}

and so on.

Once the dynamical system is reconstructed in a manner outlined

above, a recurrence plot can be used to show which vectors in the

reconstructed space are close and far from each other. More

specifically, VRA calculates the (Euclidean) distances between

all pairs of vectors and codes them as colors. Essentially, RP is

a color-coded matrix, where each [i][j]th entry is calculated as

the distance between vectors Y(i) and Y(j) in the reconstructed

series. Returning to the last example, the Euclidean distance

between vectors Y(10/9/98) and Y(10/16/98) is

Distance(Y(10/9/98), Y(10/16/98)) = [(7900-8417)^2 + (7785-7900)^2

+ (8029-7785)^2]^1/2 = 583

After the distances between all vectors are calculated, they are

mapped to colors from the pre-defined color map and are displayed

as colored pixels in their corresponding places. A recurrence

plot is essentially a graphical representation of a correlation

integral. The important distinction (and an advantage of the

recurrence plots) is that the recurrence plots, unlike the

correlation integrals, preserve the temporal dependence in the

time series, in addition to the spatial dependence.

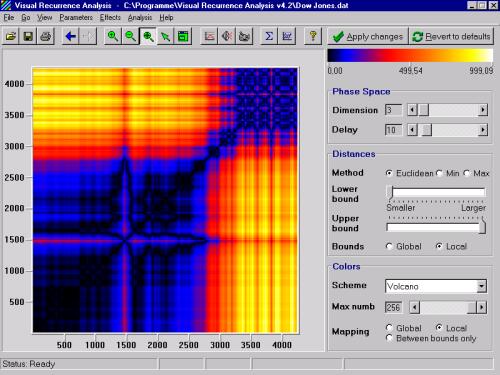

Here is an example of a recurrence plot constructed from the

weekly closing prices of the Dow Industrial Average index (file

DowJones.dat included with VRA).

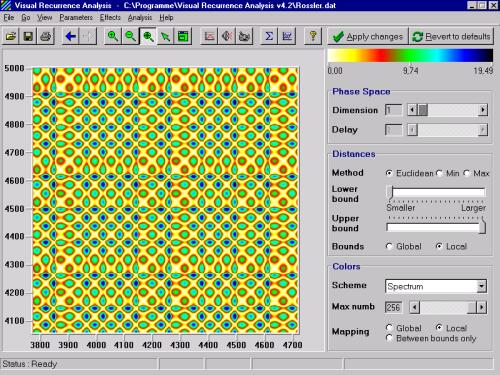

For the actual analysis and meaningful results, it is probably a good idea to use a stationary time series. Also, to make RP more meaningful, the color mapping should be meaningful, too. For example, “hot” colors (yellow, red, and orange) can be associated with small distances between the vectors, while “cold” colors (blue, black) may be used to show large distances. This way one can visualize and study the motion of the system trajectories and infer some characteristics of the dynamical system that generated the time series. Here is how the recurrence plot of the chaotic signal (Rossler attractor, file Rossler.dat included with VRA) looks like:

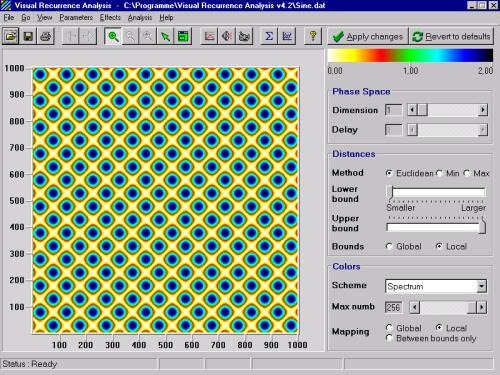

The global structure and local instability are the forces at work in the Rossler attractor, as can be seen from the recurrence plot above. Compare it with the recurrence plot of a strictly periodic signal (simple sine wave, file Sine.dat included with VRA):

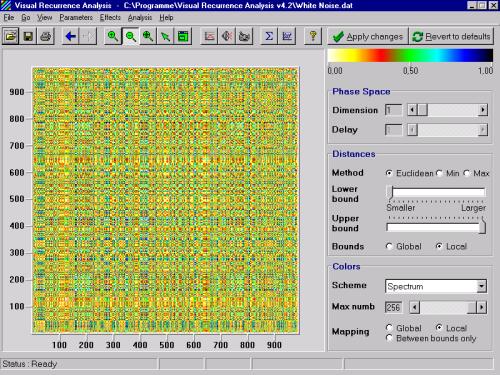

For random signals, the uniform (even) distribution of colors over the entire RP is expected. The more deterministic the signal is, the more structured the recurrence plot will be. Compare the recurrence plots above with that of the white noise time series (file WhiteNoise.dat included with VRA):

VISUAL RECURRENCE ANALYSIS HOME